Qatari LNG shutdown, US refining stocks, oil price spike, BlackRock and AES

Sunday Energy Brief - March 8, 2026

This week’s coverage

Impact of Qatar’s LNG shutdown on US producers

Why refining stocks are booming as oil prices fall

Oil price spike translates to billions for crude producers

Cheniere’s big bet on the future of Chinese LNG

Japan nuclear restart a key signal for global LNG

What BlackRock sees in power that Wall Street discounts

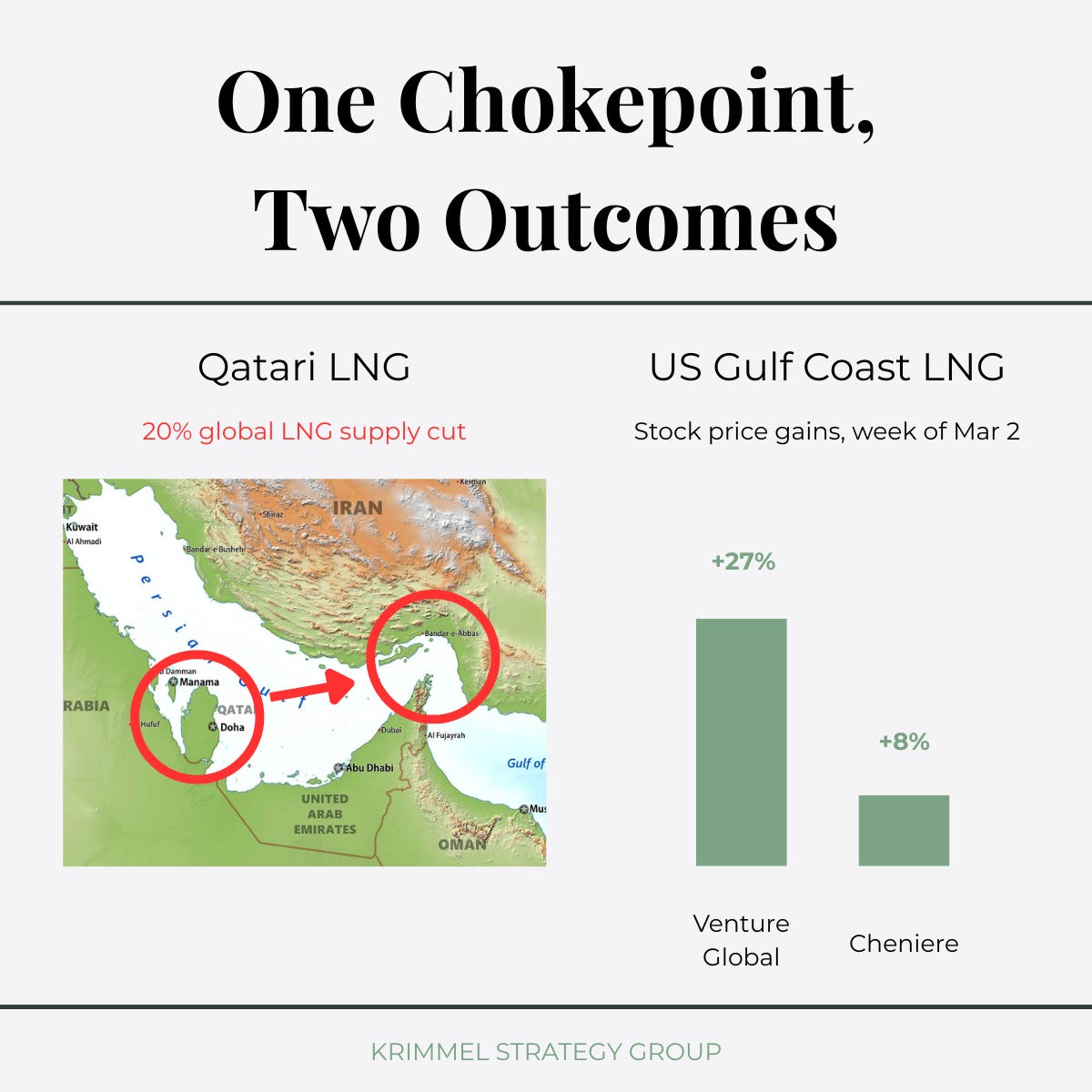

Impact of Qatar’s LNG shutdown on US producers

Qatar has shut down its entire gas liquefaction operation, taking 20% of global LNG offline due to regional combat.

This supply crunch has already caused Dutch TTF futures to jump over 60% and JKM prices to rise by 40%.

US producers like Cheniere and Venture Global are seeing significant stock gains as a result.

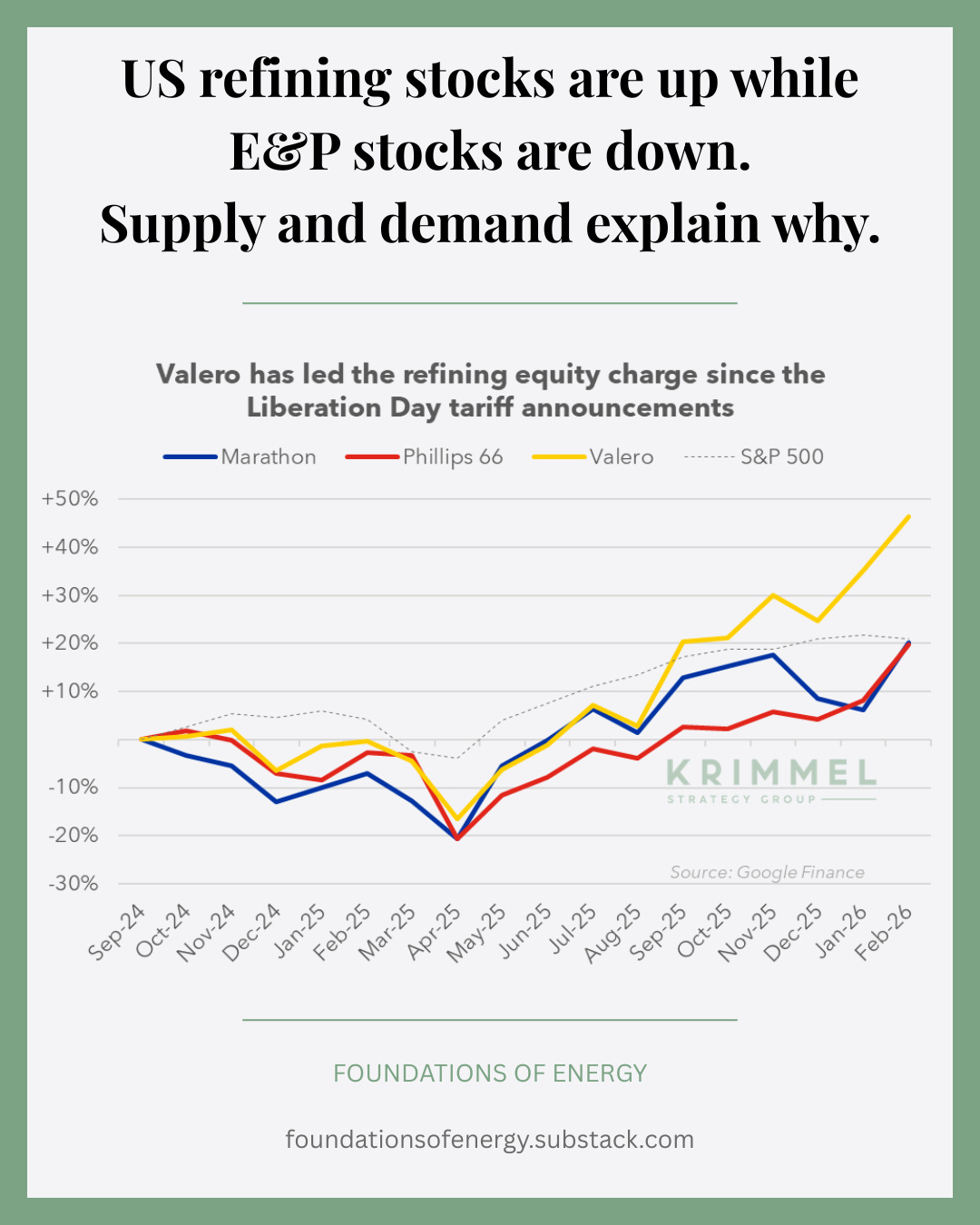

US refining stocks are up while E&P stocks are down. Supply and demand explain why.

Oil prices have been falling for over two years, yet refining stocks like Valero are booming with sizable gains since late 2024.

This divergence occurs because refiners profit from the widening price spread between crude inputs and finished product outputs, rather than just the price of oil itself.

Recent US refinery closures have further constrained product supply, boosting margins even as crude prices drift lower.

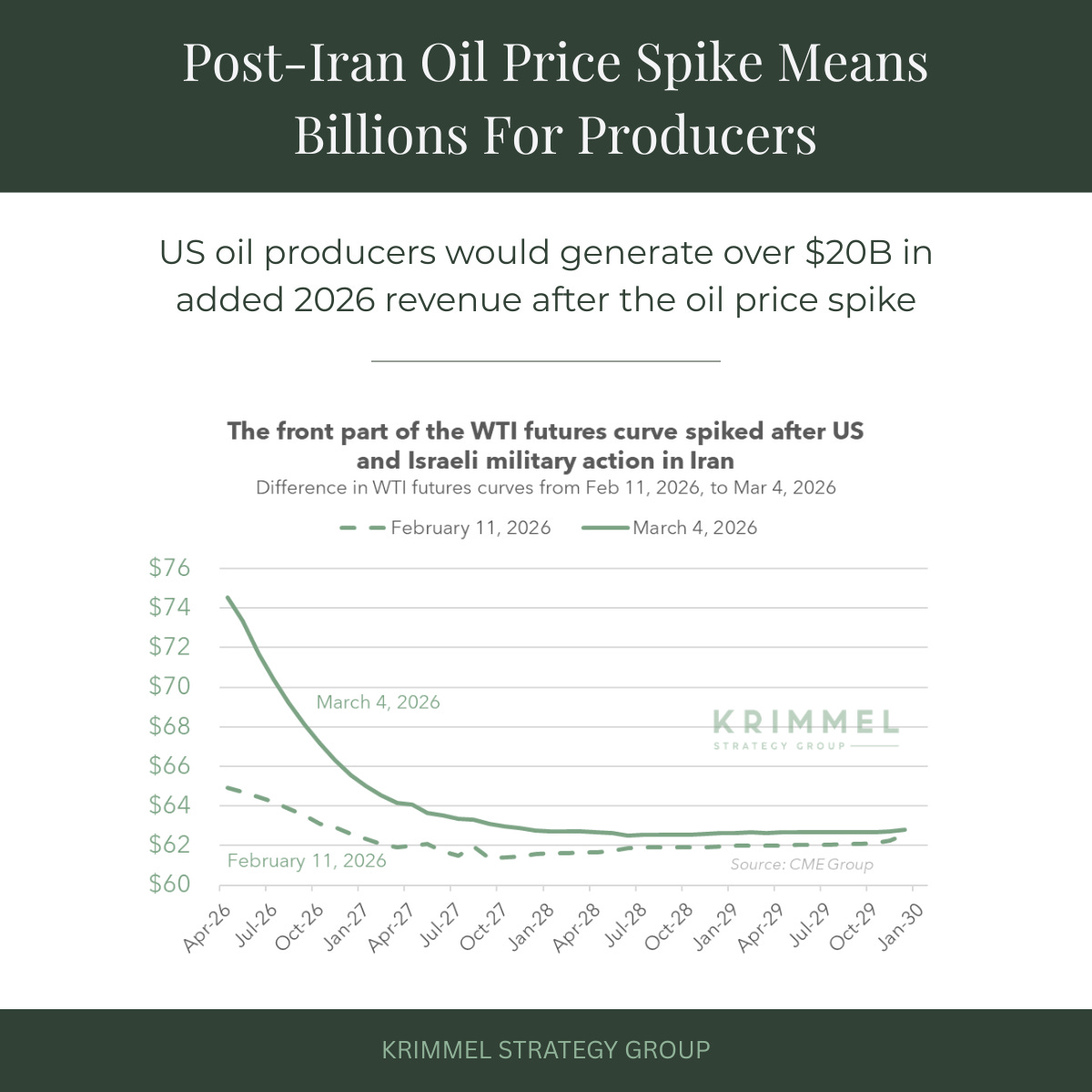

Why the post-Iran oil price spike is worth billions to US producers

Oil prices for near-term delivery have surged by $10 compared to last month.

This significant price spike could translate into over $20 billion in additional profit for US crude producers in 2026.

Many companies are now facing critical board-level decisions regarding whether to lock in these gains through hedging.

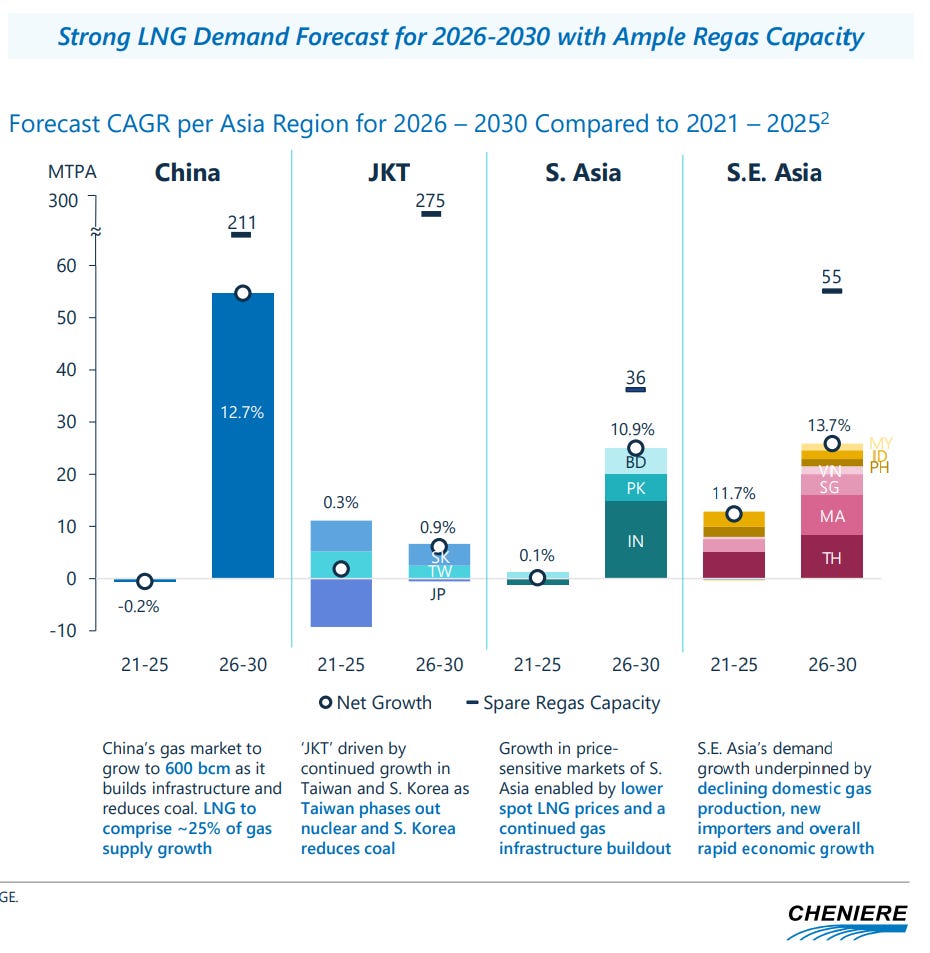

China’s LNG demand has been flat for five years but Cheniere expects that to change

China bought roughly the same amount of LNG in 2025 as it did in 2020.

Cheniere hopes that’s about to change in a big way.

For Cheniere to be right, some important macro factors all need to simultaneously break the right way.

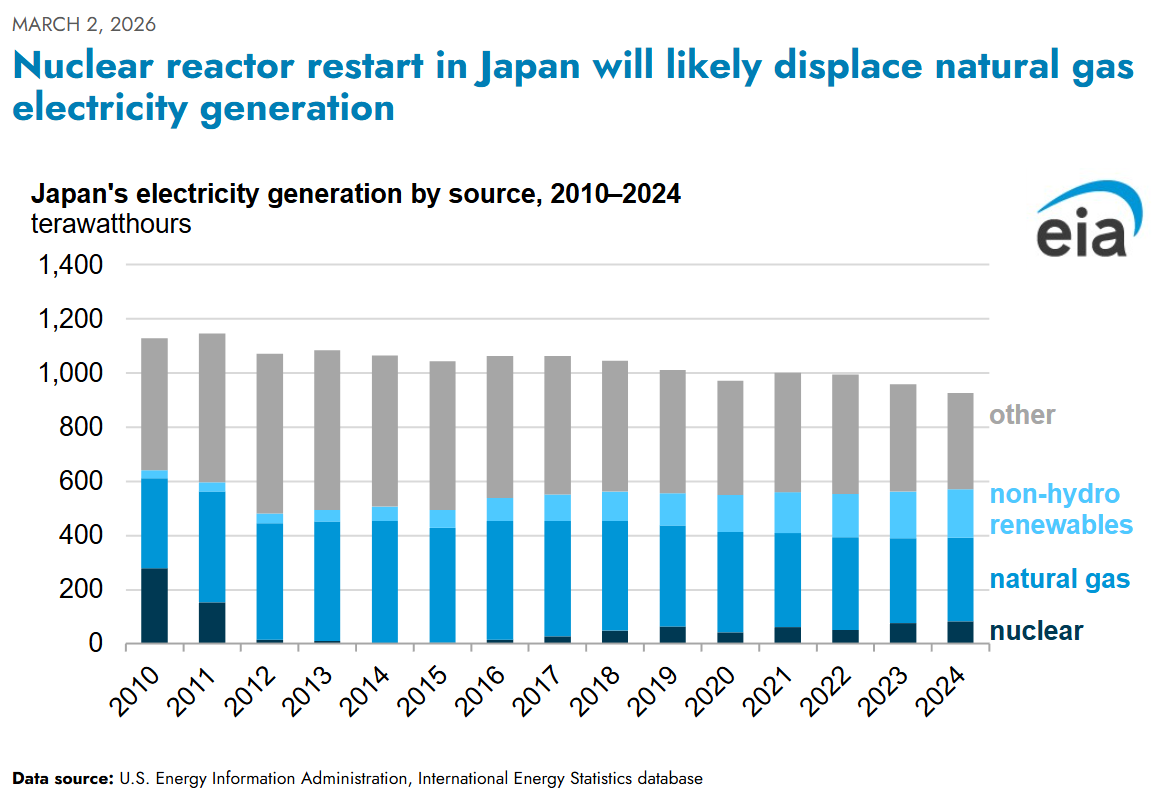

LNG developers are on notice as Japan restarts a nuclear reactor

Japan’s recent nuclear unit restart at its largest plant has global LNG developers paying close attention.

The move could displace 62 billion cubic feet of natural gas imports annually, potentially cutting U.S. exports to Japan by one-third.

This highlights a growing long-term challenge where nuclear power may emerge as a major baseload competitor to LNG.

What I’m Excited About This Week

My first experiment with OpenClaw

OpenClaw is all the rage in the tech world. It’s an AI agent that runs on your own hardware, or on a VPS in my case. But it’s not in someone else’s cloud. Right now I have it comb through energy news and score the different articles, press releases, and reports by a rubric I provide. It’s helping me high-grade my information diet, which is a fun and fascinating use case to help me build comfort in this space.

We are all coaches, and we need to tame our “advice monster”

As part of becoming a better coach, I’m reading The Coaching Habit by Michael Bungay Stanier. The overarching thesis is about how to use questions to tame your “advice monster”. His explanation for why “And what else?” is the greatest coaching question of all time was particularly powerful for me. It’s a short, impactful read, and it’ll help you better serve the people around you, whether you’re a manager, a division president, or an executive coach. I definitely recommend it.

This week’s insight

Who actually funds the power sector’s future? The AES deal is a key frame.

This week a consortium including a division of BlackRock agreed to buy AES, a large publicly traded US power generation company, for $11B, taking the company private.

In the AES press release announcing the deal, the chairman of the board laid bare the tension between public and private markets:

“In the absence of a transaction with the Consortium, the Company would likely require a plan that includes reduction or elimination of the dividend and / or substantial new equity issuances.”

Earlier in the press release, management acknowledged that the company’s “electric utilities in Indiana and Ohio are experiencing significant demand growth…”

Meeting that demand growth will require investment. And lots of it.

But public market shareholders demand dividends and share repurchases. They don’t have a lot of patience for pouring cash back into the business to meet future demand that comes with meaningful uncertainty.

That’s the tension.

Do you become a cash cow that maximizes transfers to shareholders?

Or do you invest in secular demand growth, ramping back on cash transfers to owners in the process?

With this deal, both parties get what they want: existing shareholders get a cash windfall, while new owners can exercise patience and invest for even larger returns in the future.

This week it’s a story about BlackRock and AES.

Going forward, it’s a story about what role capital markets will play in the evolution and expansion of our power sector.

Are public markets focused on near-term cash returns in a way that preempts meaningful investment for future power growth?

Are there enough private investors willing and able to deploy the billions of dollars, and wait for the years and decades of various returns horizons, to drive the power sector transformation that most observers think is critical?

And what happens with reduced visibility into these essential companies, as public reporting is replaced by private boardroom conversations without disclosure?

Capital providers are the tip of the spear when it comes to our ongoing energy transition.

As the reality around the scale of these investments sinks in, we’re seeing some capital providers step up while others step back.

Parlor games about the technology and politics of the energy transition capture the most attention.

But the question of who actually funds the work, and just how much capital and patience they really have, is even more important in understanding how our energy sector evolves from here.